Market Insight – Relief Rally and a fragile peace

Summary

- Markets bounced back, but the situation is still uncertain

Stock markets had a strong week after tensions between the US and Iran eased and oil prices fell. However, talks over the weekend didn’t lead to a breakthrough, so while the worst fears have eased, there’s still no clear resolution. - The recovery is broader, not just driven by big US tech

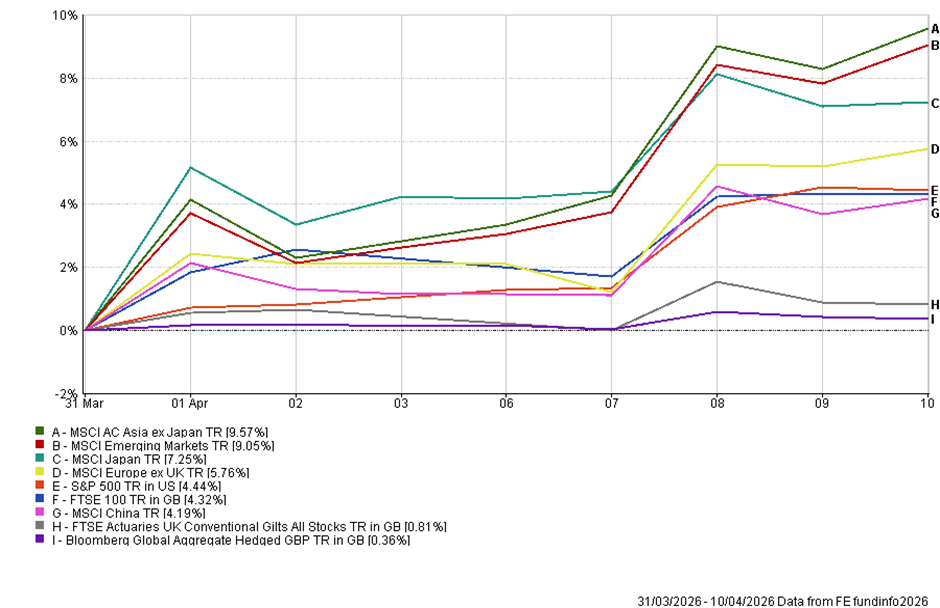

Gains have come from a wider range of regions, especially Asia and emerging markets, rather than just large US companies. This suggests investors are cautiously rebuilding confidence, but not fully committing yet. - Inflation has picked up again, mainly due to energy costs

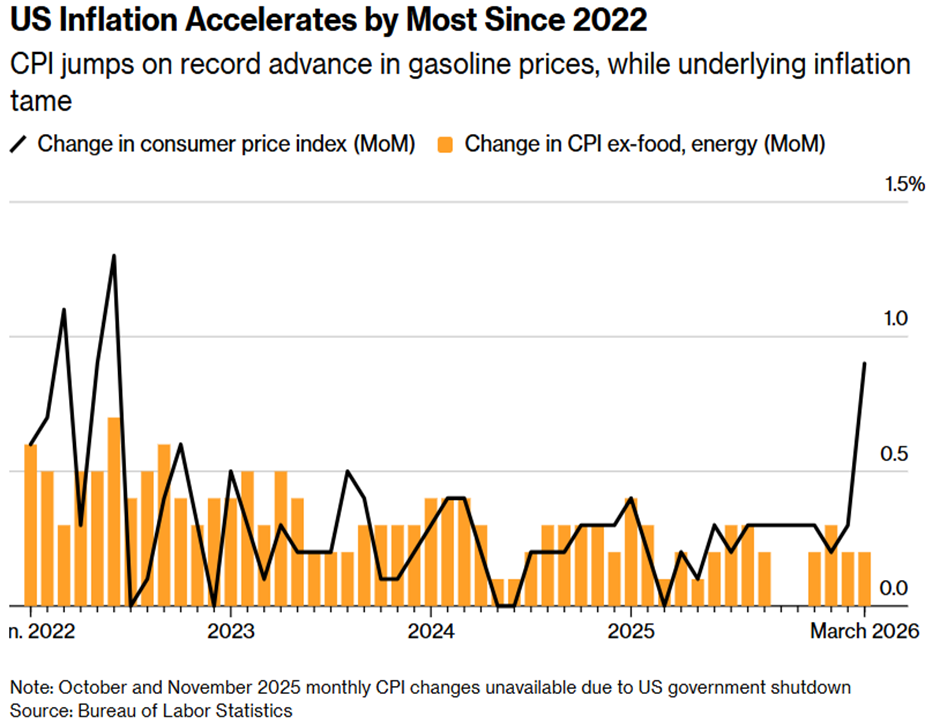

US inflation rose more than expected, largely because of higher petrol prices. While other price pressures are still relatively contained, there’s a risk that higher energy costs could spread into the wider economy if they persist. - Consumers are feeling the pressure despite stable economic data

Although employment and company earnings still look solid, consumer confidence has dropped sharply. People are increasingly worried about rising prices, which could lead to weaker spending if the pressure continues. - What matters next: oil prices and company earnings

Bond markets are signalling that interest rates may stay higher for longer. This week, company results—especially from large banks—will be closely watched to see if businesses can continue to grow despite higher costs. For markets to keep rising, investors will need to see stable energy prices and strong earnings.

Full Insight:

After a deeply unsettled March, markets finally managed a genuinely better week, helped by the announcement of a ceasefire between the US and Iran and by a sharp retracement in oil prices. The immediate sense of crisis faded, equity markets rallied strongly, and investors were prepared, at least briefly, to believe that the worst of the energy shock might already be behind us. The S&P 500 recorded its best week since November, while crude posted its biggest weekly fall since 2020.

That relief was understandable, but it never quite became a full all-clear. The rally faded a little into the end of the week, and the tone heading into Monday is more cautious again after the weekend talks between the US and Iran in Pakistan ended without agreement. The ceasefire is still holding for now, but the core disagreements remain unresolved, especially around Iran’s nuclear programme and the future of shipping through the Strait of Hormuz. Markets have therefore stepped back from pricing a true worst case, but they are not yet pricing a proper resolution either.

This month’s recovery has been impressive and, importantly, broader than many would have expected at the end of March, considering the backdrop. Asia ex-Japan has led the rebound, followed by emerging markets and Japan, with Europe also recovering well. The US has bounced too, but less convincingly, while China has lagged and bonds have barely joined in. That feels less like a simple return to the old leadership and more like a broader rotation into areas that had either been oversold on the war scare or were less exposed to the original AI-capex wobble. In that sense, the market action has actually been moderately encouraging. It suggests investors are looking past the immediate crisis and beginning to rebuild risk, but doing so selectively rather than blindly.

US Inflation & Sentiment: The inflation data helped that process, though it also underscored why the macro backdrop remains awkward. US CPI rose 0.9% in March, the largest monthly increase since 2022, taking the annual rate to 3.3%. Almost three-quarters of the monthly rise came from gasoline. Core CPI, by contrast, was relatively tame at 0.2% on the month and 2.6% on the year. So far, then, this still looks like an energy-led inflation shock rather than a broad-based reacceleration across the whole economy. That was enough to let equities breathe. But it was not enough to reassure bonds, because if oil and shipping disruption persist, today’s energy shock can still very easily become tomorrow’s broader inflation problem.

Consumer sentiment tells the same story from a different angle. The University of Michigan’s preliminary April reading fell sharply to a record low, while one-year inflation expectations jumped markedly. Current conditions fell to a record low, and the expectations component dropped to its weakest level in decades. Those are poor numbers, and are relevant because they suggest households are already feeling the squeeze from higher fuel costs. Markets may be willing to celebrate a ceasefire, but consumers are looking at petrol prices, inflation expectations and the risk to their own spending power.

That leaves the US in an awkward but not yet disastrous position. The hard economy still looks good enough that investors are not yet seriously pricing recession. Labour market data have held up, and earnings expectations remain constructive. But the risk is that real incomes start to weaken as the energy shock feeds through. In other words, the economy still looks solid enough for now, but the bridge from oil shock to weaker consumption is there if prices stay elevated.

That is why bonds remain the more interesting battleground than equities. Equities can withstand a lot if earnings remain solid and investors believe the oil shock will fade. Bonds are less forgiving because they have to process both the inflation impulse and the policy implications. Treasury yields rose after CPI, and rate markets now assign only a limited chance of a Fed cut this year. The market is no longer assuming inflation will glide back to target. It is moving toward the view that the Fed may be on hold for longer, and that feels fair enough while the Strait remains constrained and oil volatility remains high.

On the UK side, last week’s data were not especially comforting. Services activity slowed materially in March, with the composite PMI slipping closer to stagnation, while input costs rose sharply as energy, raw materials and transport costs increased. Business optimism weakened at the same time. Construction was similarly soft, with the sector still in contraction and input cost inflation hitting another high in the monthly survey. That points to the same uncomfortable mix we have been discussing for a while now: growth is slowing, but inflationary pressures are re-emerging on the cost side.

Europe looked similar. Euro area growth slowed again in March, while inflation rose, largely driven by energy. Manufacturing held up better than services, but input costs and prices charged both moved higher. So the message from Europe was also one of stagflationary pressure rather than outright collapse: weaker demand, tighter margins and renewed inflation sensitivity at the same time. Europe remains especially vulnerable in this type of environment because it takes the inflationary hit first and has a smaller growth cushion.

Trump has had enough: There is also still a political dimension to all of this. My reading remains that Trump wants out. The war is unpopular domestically, including with parts of his own base, and the combination of higher fuel prices and collapsing consumer sentiment is exactly the sort of thing the White House will be watching closely. That does not mean a deal is close, or that events are fully under Washington’s control. But it does mean there is still a strong domestic incentive to keep some diplomatic process alive even after the Pakistan talks failed. That probably remains the single biggest support for risk assets in the near term.

The other support is earnings, with analysts continuing to raise the bar, and this week, that becomes the second big driver. US banks begin reporting, starting with Goldman Sachs, followed by JPMorgan, Citigroup, Wells Fargo, Bank of America, and Morgan Stanley. Expectations are for solid results, helped by stronger trading activity through a volatile quarter. More broadly, this reporting season is pivotal because investors will want reassurance that profits are still growing strongly enough to absorb higher energy costs, sticky inflation, and the re-emergence of old questions about AI capex and margins. Earnings optimism has held up surprisingly well, which is one reason equities have been able to rally despite the macro noise.

The main message to convey is that this was a positive week overall, better than many would have anticipated at the end of March. Markets have rebounded sharply this month, fears related to the war have eased, and this recovery has broadened more healthily than just focusing on a few major US companies.

However, there is still no resolution, the Strait of Hormuz remains constrained, and the economic impacts are only beginning to show in inflation and sentiment data. This is not an indication of peace being factored in; rather, it reflects a shift from panic to a more uncertain continuation.

This week… the importance of the Middle East remains significant, especially following the weekend’s unsuccessful talks. Oil and shipping remain central to the overall economic picture. This week, however, earnings reports will take centre stage as the second major focus. The banks will provide an early indication of trading conditions, credit quality, and investor confidence after a quarter marked by concerns over war and rising energy prices.

More generally, investors will seek confirmation that earnings growth is strong enough to support markets amid higher energy costs, elevated inflation, and unstable bond markets. Since March, markets have already rebounded significantly from their lows. To maintain this upward trend, two key factors are likely needed: stability in oil prices and continued strong earnings.

Tom McGrath 12.04.2026

Edited by Ash Weston 12.04.2026