Market Insight – NVIDIA, Iran Relief and the Stagflation Test

Summary

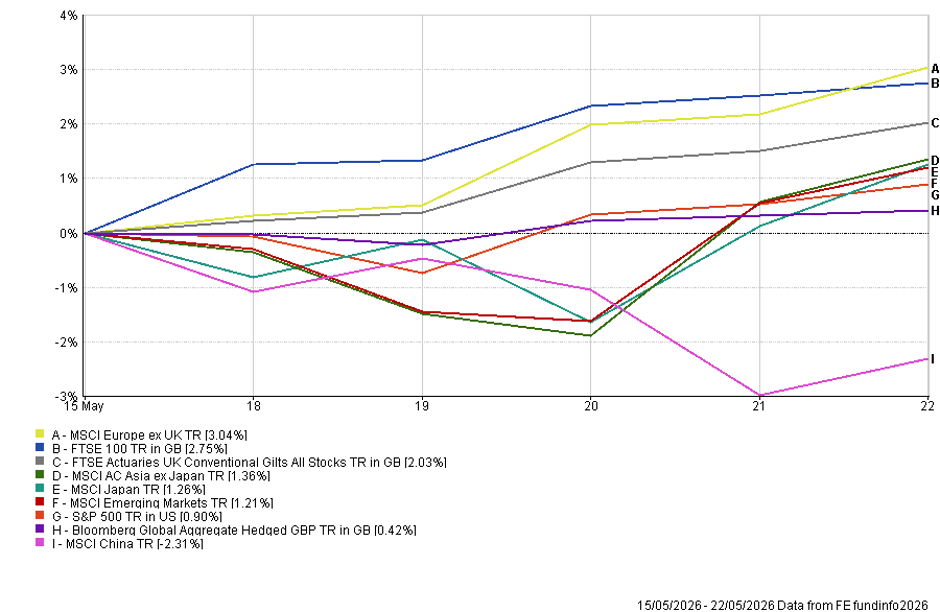

- Markets recovered as geopolitical pressure eased, but the rebound was not broad enough to signal a full all-clear. European equities rose just over 3%, the FTSE 100 gained 2.8%, UK gilts recovered around 2%, and the S&P 500 added just under 1%. China was the clear laggard, falling a little over 2%, showing that investors are willing to take risk again, but remain selective.

- NVIDIA kept the AI investment case intact. Record revenue, stronger data centre sales, good guidance, a larger buyback and a higher dividend showed that AI demand is still feeding through into real earnings and cash flow. Some valuations are high, but the rally is not just based on optimism; in many areas, it is being supported by genuine profit growth.

- The possible US–Iran off-ramp helped oil prices fall, but the inflation impact has not disappeared. Reports of a potential 60-day ceasefire extension and steps to reopen the Strait of Hormuz reduced worst-case fears. That is helpful for Europe, the UK consumer and oil-importing emerging markets, but earlier pressure on energy, transport, food and producer costs is still moving through the economy.

- Central banks remain in a difficult position. The Fed is not under pressure to hike, but sticky inflation, tariffs, energy costs and AI-related infrastructure demand make near-term rate cuts harder to justify. In the UK and Europe, weaker growth is arriving at the same time as renewed price pressure, leaving policymakers with limited room to support the economy without risking inflation credibility.

- The investment backdrop remains positive, but bond yields are the key risk to watch. AI earnings and the prospect of a Middle East de-escalation are supporting markets, while higher yields remain the main constraint. If oil continues to fall and inflation data soften, equities can move higher; if yields stay elevated, the rally becomes more fragile. For now, it makes sense to stay constructive, but not indiscriminately bullish.

Full Overview

For the first time in several weeks, the Iran conflict was not the dominant day-to-day market headline, but it remained the unresolved macro risk sitting behind almost everything else. Markets began the week in a relatively confident mood, helped by ongoing enthusiasm around AI infrastructure, semiconductors and memory stocks. However, that oIt is a hot Bank Holiday Monday in the UK, and markets have started the week in a similarly toasty mood. European equities are higher, oil is sharply lower, and investors are leaning back into risk, helped by renewed hopes that the US and Iran may be edging towards a deal that could extend the ceasefire and eventually reopen the Strait of Hormuz. After several weeks in which markets had to absorb a war-driven energy shock, higher inflation expectations and a sharp rise in bond yields, the possibility of a diplomatic off-ramp has been enough to reignite risk appetite.

Last week itself was constructive rather than euphoric. MSCI Europe rose just over 3%, the FTSE 100 gained 2.8%, UK conventional gilts recovered by around 2%, and the S&P 500 added just under 1%. Japan, Asia ex Japan and emerging markets were modestly positive. At the same time, China was the clear laggard, falling a little over 2% as domestic policy concerns and renewed pressure around capital controls weighed on sentiment. The improvement in markets was not broad enough to suggest a clean all-clear, but it did show that investors are still prepared to look through geopolitical risk when earnings momentum remains strong.

The biggest event of the week was NVIDIA, which once again delivered impressive numbers: record revenue, significantly higher data centre sales, strong guidance, an increased share buyback, and a notable dividend increase. Although the share price reaction was not extraordinary—partly due to extremely high expectations—the market significance was clear. NVIDIA demonstrated that the AI investment cycle is still translating into revenues, margins, and cash flow.

This latest performance reinforces the idea that the current equity rally is not solely driven by optimism. It is being supported by earnings upgrades, capital expenditures from hyperscalers, data centre expansion, semiconductors, networking, power infrastructure, and the broader physical infrastructure necessary for AI to function effectively.

This is why the AI debate needs to be approached thoughtfully. There is undoubtedly excitement, and certain parts of the market are expensive, but this is not simply a case of multiple expansions reminiscent of 1999. Much of the rally has been driven by actual earnings rather than investors paying higher valuations without question.

The more useful distinction is between FOMO and earnings momentum. There is some fear of missing out, but there is also genuine earnings delivery. NVIDIA is the clearest example, but the broader point is that analysts are still upgrading their profit forecasts for the parts of the market most exposed to AI compute, memory, power, and infrastructure. That is why equities have been able to withstand higher yields and geopolitical stress better than many expected.

Peace Nearing or just More Hot Air?

Reports over the weekend suggested the US and Iran are discussing a framework that could extend the ceasefire for 60 days, reopen and de-mine Hormuz, and create space for a more permanent settlement. This is clearly better than open-ended escalation, but it is not yet a resolution. Nothing has been signed, Iran has not confirmed all the US version of events, and major disagreements remain around sanctions relief, frozen assets, uranium enrichment, missile capabilities and the wider regional conflict. Markets are right to price a lower probability of the worst-case scenario, but wrong if they assume the risk has disappeared.

Oil’s reaction shows how much tension had built up in the system. Brent fell sharply on Monday morning as investors priced in a better chance that Hormuz could reopen and shipping flows might gradually normalise. That is helpful for Europe, the UK consumer and oil-importing emerging markets. But a lower oil price today does not undo the inflation already pushed into transport, food, energy bills and producer costs. It also does not immediately solve insurance, de-mining, tanker movements or supply-chain disruption. The acute shock may be fading, but the economic after-effects are still working through the system.

The US remains the most resilient major economy, but it is not immune. The Fed minutes showed a central bank that has shifted back towards concerns about inflation. Officials may not want to hike, and the bar for doing so remains high, but the old assumption that the next move must be a cut has weakened. Inflation is proving sticky, tariffs and energy are complicating the outlook, and AI itself may be adding to price pressure through memory chips, data centre construction, power demand and utility costs. The Fed can talk tough and hope that bond markets do some of the tightening for it, but the direction of travel is clear: rate cuts need more evidence, and that evidence is not yet obvious.

The US consumer is also becoming more complicated to read. Tax refunds and still-firm employment have helped cushion the hit from higher gasoline prices, and spending has not collapsed. But resilience is not the same as strength. Buffers increasingly support consumers, while lower-income households are more exposed to fuel and food costs. That creates a lagged risk. The economy can look fine on the hard data while sentiment deteriorates beneath the surface. If oil stays elevated or if bond yields tighten, financial conditions could tighten further in the second half of the year.

UK data showed significant weakness in retail sales, which fell by 1.3% in April. This decline was worse than expected and marked the sharpest drop since May 2025. Sales of motor fuel plummeted following a period of stockpiling in March. More importantly, it seems households are not redirecting their savings to other expenditures. Consumer confidence has sharply declined, especially among lower-income families, while even average-income households are relying on their savings. Wealthier individuals appear to be relatively unaffected, but the broader consumer base is feeling the pressure. This is the kind of uneven impact we would anticipate from an energy shock: it first affects essential goods, then consumer confidence, and finally discretionary spending.

The fiscal backdrop is not much help. Labour’s support package, including VAT cuts on some summer attractions, may soften the edges of the shock, but there is limited room for a large-scale response. The UK deficit has already reached its highest April level since 2020, leaving the government with little space to offset the real income squeeze without further unsettling the gilt market. That leaves the Bank of England in an awkward position. Growth is weak, but inflation risk is rising again. For UK assets, the case remains more valuation-based than growth-based: the FTSE 100 has defensive, international and dividend support, but the domestic economy is not providing much momentum.

Europe looks even more exposed to the stagflation-lite risk. The flash PMIs were poor. The eurozone composite PMI fell to 47.5, the lowest level in two and a half years, with services particularly weak. Manufacturing has been more resilient, helped by stockbuilding and front-running of supply shortages, but even that support appears to be fading. Germany remains in contraction, France’s data deteriorated sharply, and employment signals are weakening. The important point is not just that growth is soft, but that price pressures are still rising despite weak demand. Input cost inflation accelerated again, and output prices rose at the fastest pace in more than three years. That is the uncomfortable part for the ECB. European equities could enjoy a relief rally because they have been the most exposed to the shock. But structurally, Europe remains closest to the inflation-first, growth-second problem we have been highlighting.

Asia and emerging markets are more mixed. North Asia continues to benefit from the AI supply chain cycle, particularly Taiwan and Korea, where semiconductors, memory, and advanced hardware remain central to global capex. But EM as a whole is becoming less straightforward. The upside is increasingly concentrated in a small number of AI-linked names, while oil importers face pressure from higher energy costs, and some central banks may need to tighten pre-emptively to protect inflation credibility. China remains the weak link: strategically important in AI hardware, batteries, rare earths and industrial manufacturing, but still constrained by weak domestic confidence, capital controls and policy uncertainty.

For the moment, it seems the markets have two accelerators and one brake pedal. The first engine is AI earnings, and NVIDIA showed that it is still running hard. The second is the prospect of a Middle East off-ramp, which would reduce oil risk and support global risk appetite. The brake is bond yields. If oil keeps falling and inflation data soften, equities can probably move higher. If yields remain elevated because the energy shock has already broadened into producer prices, transport costs and central bank caution, the upside becomes more fragile. For now, I think it makes sense to be positioned for the rally to continue, but this is not the moment to become indiscriminately bullish and keep watching bonds. NVIDIA kept the bull case around the AI rollout alive last week. The next test is whether inflation and yields allow the rest of the market to follow.

This week…

The coming week is shortened by the UK Bank Holiday and Memorial Day in the US, but it still contains some important tests. The main focus will be on US PCE inflation, which matters more than usual after the recent repricing of Fed expectations. Markets have moved from asking when rate cuts begin to questioning whether the Fed may need to stay on hold for longer.

Another issue to watch is the potential IPO wave. Reports that SpaceX, Anthropic and OpenAI could move towards public listings add another layer to the AI story. The headline market capitalisations could be enormous, but the actual free float may be much smaller. Founders, early investors and strategic backers are unlikely to sell heavily at once, and tightly controlled share structures could limit tradable supply. The IPO wave cuts both ways. It could broaden the AI bull market, but it may also signal a more mature phase of the cycle. The key question is whether these companies bring genuine earnings visibility and cash-flow discipline, or whether public investors are being asked to pay today for very long-dated optionality.

Written by Tom McGrath 25.05.2026

Edited by Ash Weston 25.05.2026