Market Insight – Markets Enter June in Better Shape Than Expected

Summary

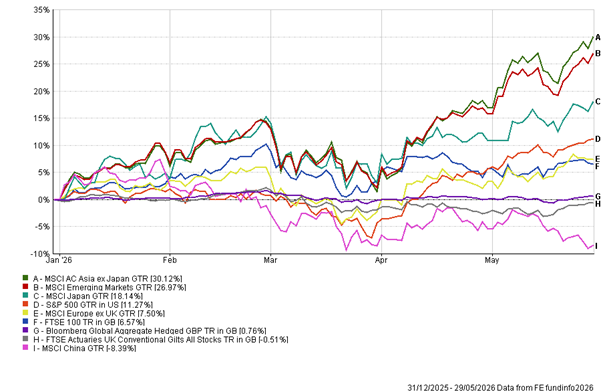

- Risk assets have continued to rise despite a difficult backdrop, with global equities higher, US markets back near record levels, and the strongest year-to-date gains coming from Asia, emerging markets and Japan rather than the S&P 500. The main support has been stronger-than-expected earnings, especially in the US, which has helped markets absorb the Iran conflict, higher energy prices and renewed inflation concerns.

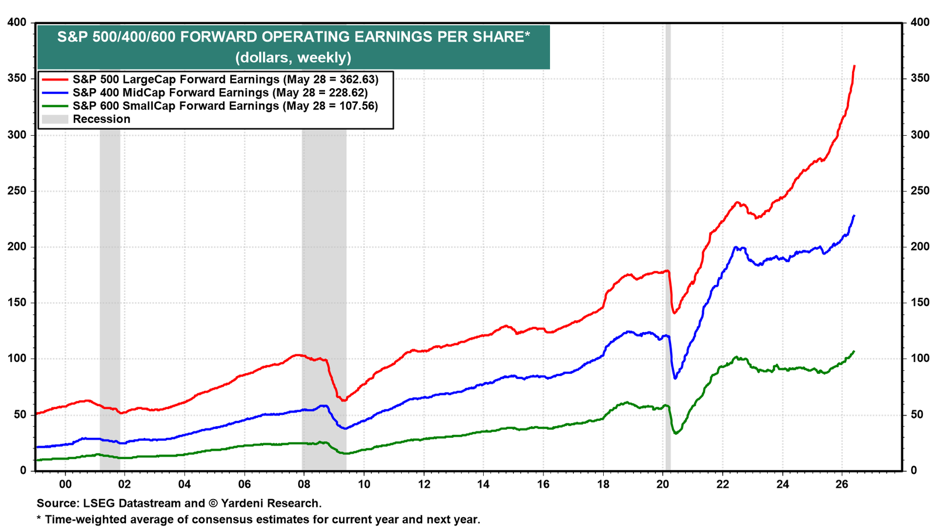

- This remains an earnings-led rally, not simply a speculative one, although parts of the AI trade now look stretched. NVIDIA’s results confirmed that AI investment remains strong, while the theme has broadened beyond US mega-cap technology into semiconductors, cloud infrastructure, networking, power equipment, industrial suppliers, copper and Asian exporters.

- Asia, emerging markets and Japan are key beneficiaries of the AI infrastructure build-out, with Taiwan, Korea and Japan increasingly viewed as essential parts of the global supply chain for chips, memory, advanced packaging and industrial automation. Japan’s story is now broader than valuation and governance reform, with AI exposure and higher domestic bond yields also shaping the outlook.

- The macro backdrop remains more challenging than equity markets suggest, with US inflation still above target, consumers showing some signs of pressure, and higher energy costs beginning to affect household budgets and corporate input costs. The Fed is therefore likely to remain cautious, while bond yields remain the main constraint on further equity market gains.

- Oil and the Middle East remain the key near-term risks, with the US and Iran appearing closer to further talks but still far from a final agreement. Markets are right to reduce the probability of a worst-case escalation, but shipping disruption, higher oil prices and delayed inflation effects mean further upside still depends on earnings delivery, stable bond yields and real progress on Iran.ted, the rally becomes more fragile. For now, it makes sense to stay constructive, but not indiscriminately bullish.

Full Overview

As we enter June, the most striking feature of markets is how strong the year has been for risk assets despite a backdrop that, in most circumstances, would have been extremely challenging. Investors have had to absorb a war in Iran, disruption in the Strait of Hormuz, higher oil and gas prices, renewed inflationary pressures, political uncertainty, and a bond market still wrestling with the idea that central banks may not be able to cut rates quickly. Yet global equities are higher, US markets are back at record levels, and the best year-to-date returns have come from Asia, emerging markets, and Japan rather than the S&P 500.

That was not the expected script at the start of the year. A direct conflict involving Iran, higher energy prices and rising inflation expectations would normally be a difficult mix for equity markets. Instead, markets have climbed through it. The reason is not that investors have ignored the risks, but that the earnings backdrop has been much stronger than feared. Corporate profits, particularly in the US, have continued to surprise positively, and analysts have been raising rather than cutting expectations. The market has therefore had a fundamental reason to look through some of the geopolitical noise.

This remains an earnings-led rally. There is some fear of missing out in the AI trade, and parts of the market are clearly extended after a strong run, but it does not yet look like a classic late-cycle bubble built solely on multiple expansion. The more convincing argument is that earnings momentum has been powerful enough to offset concerns about oil, inflation, and rates. Technology remains the clearest example, but the AI infrastructure build-out has supported a wider group: semiconductors, cloud platforms, networking, power equipment, industrial suppliers, copper and selected Asian exporters.

This time, earnings are supporting market moves: That is why the comparison with the late-1990s technology bubble needs care. There are obvious similarities in sentiment: investors are excited about a new technology, capital is flowing rapidly into the theme, and the biggest winners are beginning to dominate index returns. But there is also a major difference. In 1999, valuations ran far ahead of earnings. Today, the better companies are already generating strong revenue, cash flow, and profit growth. NVIDIA’s results were the clearest confirmation of that, but the wider message from earnings season was that the AI capex cycle remains real and is still broadening.

Asia & Emerging Markets: This also helps explain why the US market has reached fresh highs, but has not been the only story. Asia ex Japan and emerging markets have been among the strongest areas year to date, helped by the globalisation of the AI supply chain. The AI theme is no longer simply about US software platforms and the Magnificent Seven. It is increasingly about the physical layer: foundries, memory, advanced packaging, chips, networking, power, cooling, grid investment and industrial automation. Taiwan, Korea and Japan are now being treated as critical infrastructure markets for the next phase of the AI cycle.

Japan: has benefited from the same structural forces, although the story there is becoming more nuanced. The Nikkei has been helped by semiconductor and AI-related enthusiasm, while broader TOPIX performance has been less spectacular. Corporate reform, better capital discipline and improving shareholder returns remain important positives, but higher JGB yields, yen intervention, and the Middle East shock complicate the near-term outlook. Japan is no longer just a cheap reform story; it is now partly an AI supply-chain story, partly a governance story and partly a rates story.

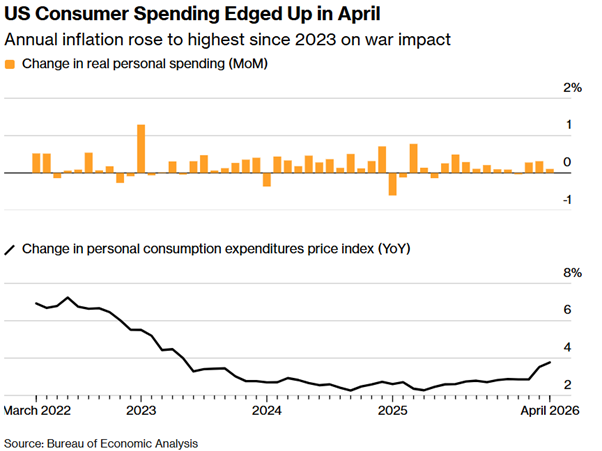

US Inflation: The macro picture is less comfortable than the equity market alone suggests. In the US, last week’s PCE data gave investors some relief, as the monthly core reading was slightly softer than feared. But the annual inflation numbers remain too high, and the details on the consumer were not especially reassuring. Real spending is still positive, but only just. Real disposable income is under pressure, the savings rate has fallen sharply, and higher fuel prices are beginning to matter. The US consumer is not collapsing, but the cushion is thinner than it was.

That distinction is crucial for the Fed. The central bank does not need to panic, but neither does it have the evidence needed to pivot dovishly. Inflation is still above target, oil prices have already fed into household budgets, and there are signs that higher input costs are moving through parts of the corporate sector. At the same time, the labour market is no longer so hot that the Fed can ignore growth risks. The likely result is a cautious, data-dependent Fed that would rather talk tough and let financial conditions do some of the work than rush into either cuts or hikes.

Bond Markets: The market can live with higher-for-longer rates if earnings keep rising. It would struggle if inflation reaccelerated and yields rose materially. That is why the bond market remains the key constraint on the equity rally. Treasury yields have eased from their most worrying levels, and gilts have also enjoyed a better period. In the UK, the gilt rally probably reflects a mix of global yield relief, softer inflation fears and a slight easing in political anxiety. The UK remains fiscally constrained, but recent political positioning has at least avoided the impression of a rapid move towards unfunded spending.

The UK: equity market case remains stronger than the domestic economic case. International earnings, energy, financials, defensives and low valuations have helped the FTSE 100. But the local economy remains fragile. Households are under pressure from energy and food costs, public finances are stretched, and consumer confidence is uneven. UK equities can still perform as a value and income market, but a powerful domestic growth story is absent at present.

Europe: faces a similar challenge, but with greater energy sensitivity. The region benefits quickly if oil prices fall and the Iran risk premium fades, but the underlying data remain soft. Recent business surveys point to weak activity, particularly in services, while price pressures remain uncomfortable. Europe remains closest to the stagflation-lite problem we have been highlighting: weak growth, rising input costs and limited room for the ECB to look through the shock. A durable Iran deal would be a genuine relief for Europe. A prolonged negotiation would keep the region vulnerable.

The Middle East remains the most important geopolitical variable. The newsflow is better than it was, but still messy. The US and Iran appear to be inching towards a tentative ceasefire extension and further talks, but there is no final agreement. Trump wants an exit, but he also needs to satisfy red lines around Hormuz, uranium and Iran’s nuclear programme. Iran wants sanctions relief and access to frozen assets. Republican hawks are pushing back against anything that looks too soft. Both sides have reasons to keep talking, but also reasons not to concede too quickly.

Markets are probably right to reduce the probability of a worst-case escalation. The conflict has become more about bargaining than uncontrolled military expansion. But it is too early to price a clean resolution. Shipping through Hormuz remains irregular, oil prices are still materially higher than before the conflict, and the economic effects are working through with a lag. Even if an agreement is reached, it will take time for energy markets, insurance costs, shipping routes and confidence to normalise.

Oil remains the hinge point. If crude prices continue to fall, the pressure on consumers and central banks should ease, helping Europe, Japan and oil-importing emerging markets in particular. If oil stays elevated, the second-round effects become more important: transport, food, producer prices, corporate margins and real incomes. This is why the market’s optimism is understandable but still conditional. The broader conclusion is that markets have entered June in better shape than expected because earnings have beaten geopolitics. AI capex, technology profits, energy upgrades and improving earnings breadth have offset inflation anxiety and war risk. That is constructive. But it also means the bar is higher. After such a strong move, investors need continued earnings delivery, stable bond yields and further progress on Iran to justify the next leg higher.

Stay Invested: With strong momentum in the markets and a genuine possibility of a peace deal in the Middle East, it may be unwise to stand in the way of markets heading higher. Relief over Iran, lower oil prices, and continued earnings upgrades could easily drive risk assets higher. Interestingly, the moment to exercise caution might be when the positive geopolitical news actually arrives. While a peace deal would be beneficial, it could also crystallise the optimism already reflected in prices. In other words, although the rally may still have room to grow, the best news could also be the point at which maintaining discipline becomes most crucial.

This week…

The first week of June should give markets a clearer test of the current narrative. In the US, ISM manufacturing and services surveys will show whether activity is still holding up amid higher energy costs and tighter financial conditions. ADP employment and Friday’s non-farm payrolls report will be the main labour-market focus. A moderate jobs number would probably suit markets best: strong enough to avoid recession fears, but not so strong as to push yields higher again.

In Europe, flash inflation data will matter because the ECB is already facing weak activity and renewed price pressure. If inflation remains sticky while growth surveys stay soft, the stagflation-lite concern will become harder to dismiss. In China, private-sector PMIs should provide a clearer picture of whether activity is stabilising after recent softness in official data.

On the corporate side, Broadcom earnings will be closely watched as another test of the AI infrastructure cycle. After NVIDIA’s results, investors will want evidence that demand for semiconductors, networking and data-centre infrastructure is still broadening. Geopolitics will remain in the background, but still central: any concrete progress on Iran, Hormuz and oil flows would be taken positively, while another breakdown in talks would quickly bring inflation and energy risk back to the front of the market’s mind.

Tom Mcgrath 31.05.2026

Edited by Ash Weston 31.05.2026