Market Insight – New highs, a closed strait & the next moves for Iran…

Summary

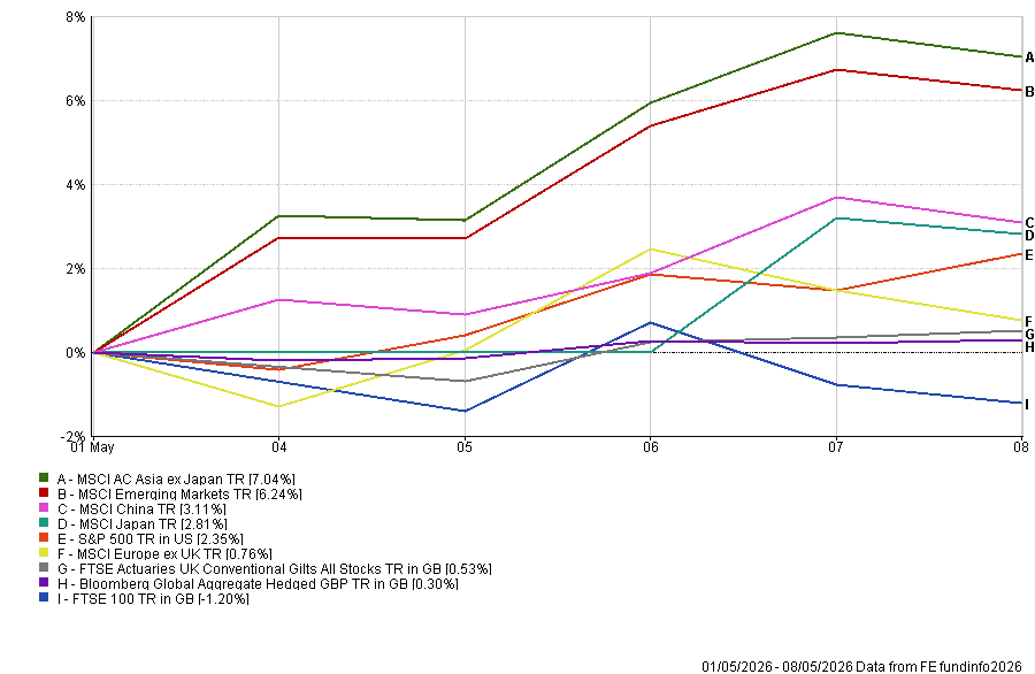

- Markets rose last week despite the Strait of Hormuz remaining unresolved. Asia led the move, with MSCI AC Asia ex Japan up about 7.0%, Emerging Markets up 6.2%, China up 3.1%, Japan up 2.8%, and the S&P 500 up 2.4% to a new high. Europe ex UK was mildly positive, the FTSE 100 fell about 1.2%, and bonds were slightly positive.

- Investors are assuming the Iran disruption can be contained, but that remains a key uncertainty. Trump’s proposal is aimed at reopening Hormuz first, although Iran appears in no rush to respond and Brent oil near $100 shows markets are still pricing ongoing risk. The danger is that markets see this as short term, while Iran may be thinking more strategically.

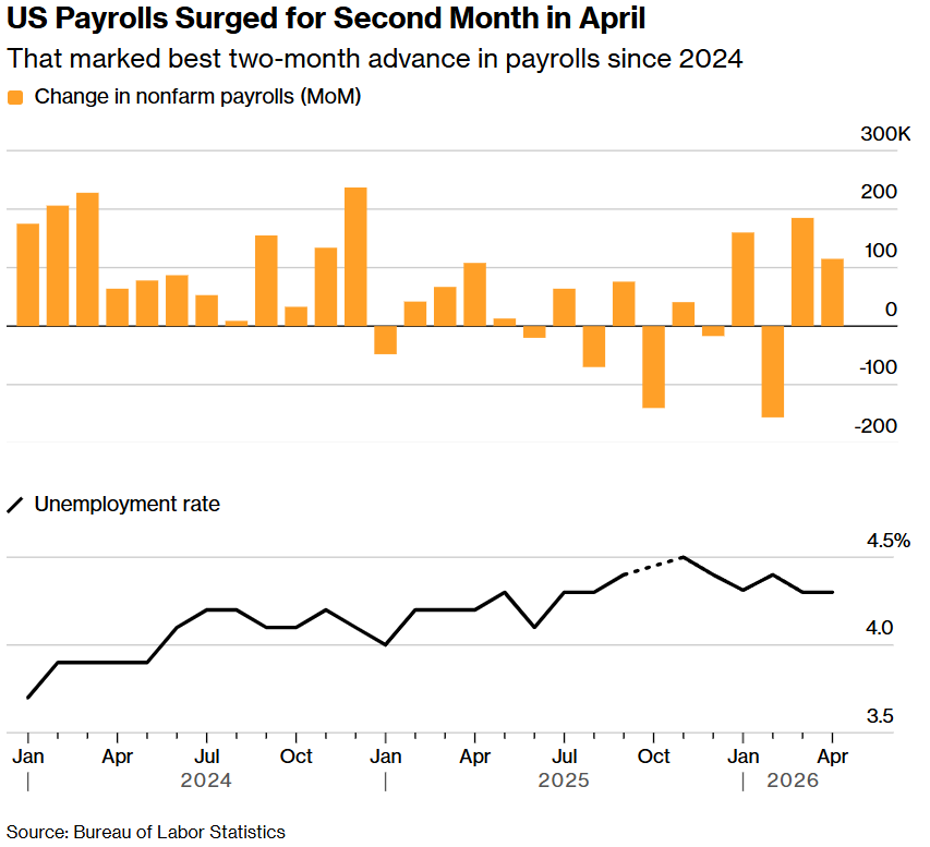

- The US is holding up relatively well. Payrolls rose by 115,000 in April and unemployment stayed at 4.3%, which gives the Fed room to wait. But the consumer backdrop is softer: sentiment has fallen sharply, petrol is above $4.50 per gallon, and pressure is building most clearly on lower-income households.

- Equities are still being supported by strong earnings and by a wider AI story. Earnings have continued to beat expectations, forecasts for 2026 and 2027 are still being revised higher, and investors are increasingly backing the companies enabling AI, including chipmakers, memory producers and infrastructure suppliers. That helps explain the strong performance in Korea, Taiwan and parts of emerging markets.

- The UK and Europe look more exposed if energy pressure persists. UK politics has not yet unsettled markets, but weaker growth, higher fuel costs and limited room for rate cuts leave little margin for policy mistakes. Europe is the clearest developed-market energy casualty if oil stays high.

This week, the key watchpoints are US inflation, Iran’s response, the Trump-Xi meeting and whether AI-related market leadership continues.

Last week was another reminder that markets do not always behave as the news flow suMarkets remained strikingly resilient last week, even as the Iran war and disruption through the Strait of Hormuz continued to dominate the macro backdrop. The S&P 500 rMarkets moved higher last week despite the continuing stalemate around the Strait of Hormuz. Asia led the advance, with MSCI AC Asia ex Japan up around 7.0% and MSCI Emerging Markets up 6.2%, driven heavily by the AI hardware and memory trade. China recovered by around 3.1%, Japan gained 2.8%, and the S&P 500 rose 2.4% to a fresh all-time high. Europe ex UK was modestly positive, while the FTSE 100 lagged, falling around 1.2%. Bonds were mildly positive.

The striking feature is that markets are behaving as though the Iran shock is manageable, even though there is still no clear resolution. The US is waiting for Iran’s response to Trump’s latest proposal, which would see Iran reopen the Strait of Hormuz while the US eases its blockade on Iranian ports. The plan appears deliberately narrow: reopen the strait first, then leave the harder nuclear questions for later. That makes sense from a market perspective, because the immediate global issues are shipping, fuel, fertiliser, plastics, aviation, and supply chains rather than the wider political settlement.

Iran, however, appears to be biding its time. Trump clearly wants a deal before he meets with Xi Jinping in Beijing, but Iran has little reason to move quickly if it believes economic pressure on the US, Europe and Asia will continue to build. Oil has come off its highs but remains elevated, with Brent still around $100. That suggests markets are pricing some chance of de-escalation, but not a durable return to normal. The danger is that investors are treating Hormuz as a short-term negotiation problem, while Iran may now see it as a longer-term strategic lever.

The US has absorbed the shock better than other regions. April payrolls rose by 115,000, and the unemployment rate held steady at 4.3%, giving the Fed room to stay patient. The labour market is not booming, but it is proving harder to break than many feared. Hiring has broadened beyond healthcare, with transport, warehousing and retail showing strength. The data-centre build-out may also be supporting construction demand, reinforcing the view that AI investment is now feeding into the real economy.

The consumer picture is more fragile beneath the surface. University of Michigan sentiment fell to a fresh record low, with gasoline prices the central concern. Petrol has moved above $4.50 a gallon, up more than 50% since the start of the Iran war, and consumers’ assessment of their current finances has fallen to the weakest level since 2009. The US economy remains resilient, but the pressure is moving lower down the income spectrum. Jobs, markets and wealth effects still support higher-income households; lower-income households are more exposed to fuel, food and borrowing costs.

The reason equities can still look through this is earnings. This is not simply a valuation-led rally or naive optimism. The latest reporting season has been exceptionally strong, with a high proportion of S&P 500 companies beating expectations and aggregate earnings growth being revised sharply higher since the end of March. Analysts have continued to lift 2026 and 2027 earnings forecasts, even through the Middle East uncertainty, underlining the improvement in the profit cycle.

The AI story is also becoming broader and more investable. Initially, the trade was dominated by the Magnificent Seven and the hyperscalers. Now investors are recognising that every dollar of AI capex flows through a wider supply chain before it reaches a data-centre rack. Semiconductors, high-bandwidth memory, networking, storage, photonics, cloud infrastructure and power infrastructure are all central beneficiaries. The strength in Micron, SK Hynix, Samsung, TSMC and ASML reflects this shift. Investors are no longer just buying companies promising AI; they are buying the companies enabling it.

This explains the strength in Asia and emerging markets. Korea and Taiwan are increasingly trading as AI infrastructure markets, not simply regional equity markets. Samsung and SK Hynix are being driven by high-bandwidth memory demand, which remains a bottleneck for AI training and inference. TSMC remains central to leading-edge chip production, while ASML controls a key lithography chokepoint. EM earnings momentum is improving, but much of the strength is concentrated in Taiwan and Korea through AI hardware, and in commodity-linked markets that benefit from higher real asset prices. This is positive, but it is not a broad EM recovery. Oil-importing economies remain vulnerable where energy costs feed into inflation, currencies and external balances.

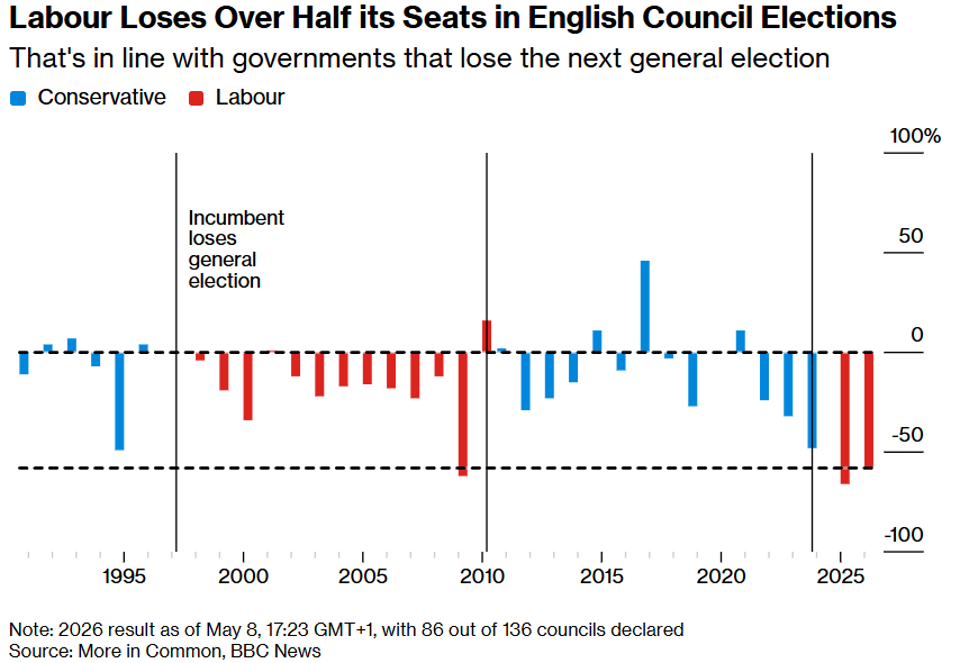

The UK deserves more attention this week. Labour’s heavy local election losses have increased pressure on Keir Starmer, but the immediate market reaction was calm. Sterling did not move significantly, and gilt yields actually fell. That suggests investors had largely priced in a poor political outcome and are not yet treating it as a fiscal event. The bigger risk is what comes next. If a weakened government or leadership challenge creates pressure for looser fiscal policy, the gilt market may become less forgiving.

The UK macro backdrop is already difficult. Higher fuel prices are squeezing households, growth remains soft, and the Bank of England is trapped. The government would like to cut rates, but imported energy inflation makes that harder. The risk is not that politics immediately destabilises markets, but that political weakness collides with higher inflation, fiscal constraint and poor consumer confidence.

Europe remains the most exposed developed region to the energy shock. Growth is weaker, energy dependence is higher, and the ECB has less room to ignore inflation pressure. If Hormuz reopens durably, Europe could bounce sharply, particularly industrials, autos and travel. But if oil remains high, Europe is where the stagflation risk is clearest.

China matters this week less because of domestic momentum and more because of the Trump-Xi meeting. Beijing has called for Hormuz to reopen and may have influence over Tehran. If Trump and Xi can present some coordinated pressure or diplomatic progress, that would support risk assets, China’s internet and Asian technology. If the meeting instead revives tariff or technology tensions, it could quickly challenge the current risk-on tone.

Looking ahead, US inflation data will be the key test. Markets are assuming the oil shock can be contained and that earnings strength can keep carrying equities higher. CPI will help show whether that remains plausible. Investors will also watch Iran’s response to Trump’s proposal, progress on the Trump-Xi meeting, Fed commentary following the recent policy split, and whether AI hardware leadership in Korea, Taiwan, and US semiconductors continues.

The overall message remains cautiously constructive, but with a narrower margin for error. Markets are not rising on thin air: earnings delivery has been strong, AI capex is still accelerating, and forward estimates continue to move higher. The bull case is that this becomes a self-reinforcing cycle, where hyperscaler spending drives semiconductor, memory, cloud, data-centre, and infrastructure revenues, which in turn support margins, profits, and equity leadership. But the macro backdrop is far from clean. Hormuz remains unresolved, oil remains elevated, and the longer that persists, the greater the risk that the shock broadens beyond energy into transport, food, input costs and consumer confidence. The rally can continue, but it now depends on two assumptions: that AI-related earnings keep validating higher valuations, and that the Iran shock remains contained rather than becoming a persistent drag on inflation, consumers and policy.

For now, markets are giving the earnings cycle the benefit of the doubt. That may be right, but it argues for selectivity rather than complacency.

Written by Tom McGrath 10.05.2026

Edited by Ash Weston 10.05.2026