Market Insight – Earnings Trump Geopolitics, For Now

Summary

- Markets Ignoring Bad News (For Now)

Even with ongoing conflict in the Middle East and political tensions in the US, stock markets continued to rise. Investors are focusing less on the headlines and more on company performance, assuming the situation isn’t getting significantly worse. - Companies Are Beating Expectations

Many large companies are reporting stronger-than-expected profits, which is helping push markets higher. However, this has also made markets more expensive, meaning there’s less room for disappointment if conditions worsen. - Technology and AI Still Leading the Way

Technology companies—especially those linked to artificial intelligence—continue to drive market gains. Strong demand for AI-related products is keeping investor confidence high, particularly in the US and parts of Asia. - Consumers Are Starting to Feel the Pressure

In the US, people are becoming more worried about the economy, especially due to rising fuel costs and inflation. While spending hasn’t dropped yet, confidence is weakening, which could become a concern later. - Risks Are Building Beneath the Surface

In the UK and Europe, rising costs and weaker growth are creating a difficult environment. Markets are currently holding up, but they could become more volatile if energy prices rise further or if company results start to weaken. The next few weeks will be key in testing how resilient markets really are.

Last week was another reminder that markets do not always behave as the news flow suggests. On the face of it, the backdrop remained deeply unsettled. The Iran conflict still had no durable resolution, the Strait of Hormuz remained only partially functional, US consumer confidence weakened sharply under the weight of higher fuel costs, and the weekend ended with two destabilising headlines: Donald Trump cancelling the planned Pakistan trip by Steve Witkoff and Jared Kushner, and topped off with the shocking shooting incident around the White House Correspondents’ Dinner.

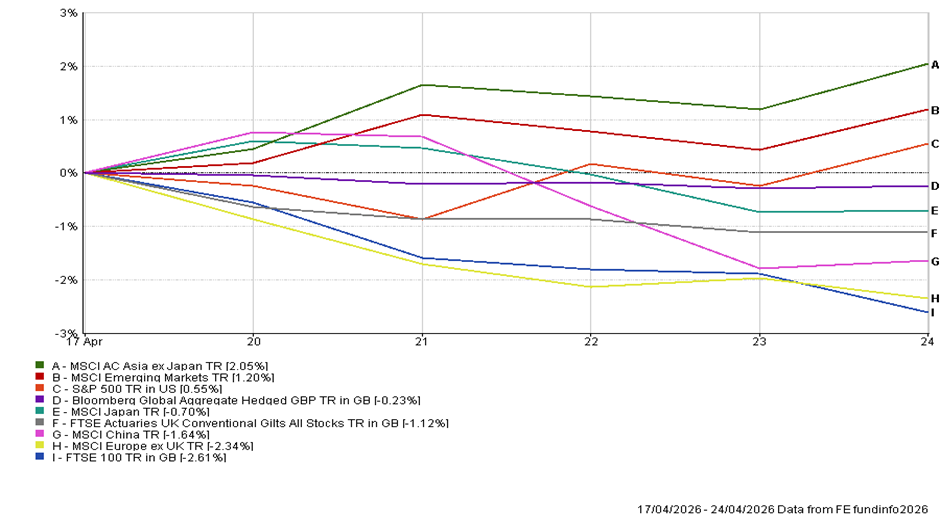

Yet by Friday’s close, equities had largely pushed higher, with the S&P 500 and Nasdaq both finishing at record highs. The performance picture over the week was striking. Asia ex-Japan led, broader emerging markets also advanced, the S&P still finished positive, while China lagged the wider EM complex, and bonds were soft.

That was not the pattern of a market hunkering down. It was a selective but surprisingly confident risk-on move, and the real question was why investors were willing to look through so much unresolved geopolitical risk. The answer, at least for now, is that markets spent most of last week treating Iran not as a fresh shock, but as a lingering drag. Before Friday’s close, there had been no obvious new military escalation, and the White House was still signalling that another diplomatic push via Pakistan remained possible.

That seemed enough for investors to conclude that stalled diplomacy was not the same thing as outright collapse. The more negative turn only arrived after markets had shut, when Trump abruptly called off the trip, complained that too much time had been wasted, and openly questioned whether anyone in Tehran was really in charge. It would not be surprising if markets are forced to confront that reality a little more honestly at the start of this week, particularly if oil opens firmer and equities a shade weaker.

Earnings Resilience: What is perhaps most surprising is how resilient equities have been, and the main explanation is earnings. Just over a quarter of the S&P 500 has now reported, with 84% beating estimates and aggregate earnings coming in 12.3% above expectations, pushing blended first-quarter earnings growth up to 15.1% from 13.0% a week earlier and revenue growth to 10.3%, the strongest since the third quarter of 2022. The strength has been broad, with industrials, technology, healthcare and materials all contributing, giving investors a genuine reason to keep adding risk despite elevated oil prices and an unresolved Middle East backdrop. The caveat is valuations: the forward 12-month P/E has risen to 20.9, well above both its five-year and ten-year averages, so while earnings are doing much of the heavy lifting, markets are paying up for that resilience and leaving themselves less room for error if geopolitics deteriorate or higher energy prices start to bite more clearly.

Technology and AI-related names were again at the centre of market moves. In the US, semiconductor shares were supported by strong results and upbeat guidance, with Intel among those helping sustain optimism. In Asia, the story was even more striking. TSMC raised its outlook on the back of robust AI demand, while SK Hynix reported a five-fold jump in quarterly profit and reiterated plans to increase spending. Samsung also delivered a sharp profit rebound. That combination matters. It suggests that investors are still prepared to believe the AI capital spending cycle remains intact, even with oil higher and the geopolitical backdrop unresolved. It also helps explain why Asia ex-Japan led the performance table and why broader emerging markets outperformed, even though China itself lagged. Last week’s strength was not really about confidence in peace. It was about confidence that earnings, especially in semiconductors and AI infrastructure, were strong enough to carry markets forward anyway.

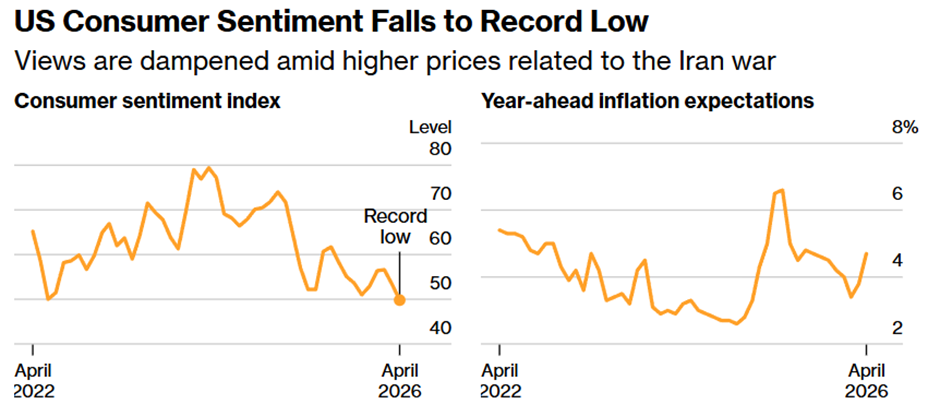

US Consumer Confidence: That makes the weakness in US consumer confidence all the more notable. The University of Michigan’s final April sentiment index fell to 49.8 from 53.3 in March, the lowest reading in the history of the series. One-year inflation expectations jumped to 4.7% from 3.8%, while longer-term expectations also moved higher. That is plainly an uncomfortable signal. Yet the reason markets brushed it aside is that hard activity data have not yet rolled over in the same way. Retail sales earlier in the week were still firm, and investors chose to trust spending and earnings over sentiment. That may turn out to be too relaxed. The more important point is that the Iran shock is now clearly showing up in household psychology through petrol prices and inflation fears, even if equity markets are not yet fully pricing it in.

The UK offered a similar kind of tension. April’s flash composite PMI rebounded to 52.0 from 50.3, which on the surface looked reassuring and came in above expectations. But the detail was less convincing than the headline. Some of the strength appears to have reflected firms bringing forward orders and working through backlogs in anticipation of future supply disruptions and higher prices. At the same time, cost pressures accelerated sharply. So the UK data were not weak enough to offer the Bank of England much comfort on growth, but they were hot enough to keep inflation concerns very much alive. That remains the right framework for the UK: inflation first, growth second. Activity is holding up, but not particularly convincingly, while price pressures are becoming harder to ignore.

Europe looked softer still. The euro area slipped back into contraction in April as costs surged, and Germany’s private sector contracted for the first time in nearly a year, with services particularly weak. That fits the broader story we have been carrying for some time: continental Europe remains the developed market most exposed to a prolonged energy shock because of its weaker growth base, greater sensitivity to imported energy costs and tighter policy constraints. Last week’s market action reflected that. Europe did not participate in the rally to anything like the same degree as the US or Asia, and the softer survey backdrop helps explain why.

So the broad message from last week is that markets were stronger than the fundamentals of the geopolitical situation alone would justify, and much more willing to give earnings the benefit of the doubt than might have been expected. That resilience has been impressive, though I’m not entirely comfortable with it. Investors appear to have concluded that as long as the conflict remains contained, however messily, and as long as company results continue to come in strongly, risk assets can keep pushing higher. That may hold for a little while longer, but the window is closing. It does leave the market vulnerable if the diplomatic backdrop deteriorates further or if higher oil prices start to bite more visibly into growth and margins. The clock ticks are becoming much more ominous.

This week… the immediate focus will remain on the same two forces that carried markets last week: earnings and central banks. On earnings, around 180 S&P 500 companies are due to report this week, so the market will get a much broader test of whether the strong start to the season can be sustained. On central banks, the Bank of England and the ECB both meet on 30 April. The most likely outcome in the UK is still a hold, but the tone will matter because the inflation signal is becoming more uncomfortable even if growth remains fragile. The ECB meeting should also help clarify how European policymakers are thinking about an energy shock that is already landing on a relatively weak regional economy. The week ahead is still less about any clean resolution in Iran than about whether strong earnings and cautious central banks can continue to outweigh higher oil, weaker sentiment and a diplomatic picture that remains plainly messy.

Tom McGrath 27.04.2026

Edited by Ash Weston 27.04.2026