Market Insight – Earnings Strength Meets Hormuz Uncertainty

Summary

- Markets stayed firm even though the backdrop became more difficult. The S&P 500 made new highs, helped by strong US earnings and continued leadership from large technology companies, while most other regions were quieter as investors worried about weaker growth, higher energy prices and policy uncertainty.

- The Strait of Hormuz is still the main issue to watch. Disruption to shipping has continued even after the ceasefire, which means energy markets remain exposed and a geopolitical premium is likely to stay in oil prices. The note makes clear that this is a serious economic risk, not just another short-lived geopolitical headline.

- Higher oil prices are making life harder for central banks. Rising energy prices push inflation up first, then start to weaken consumer spending and growth. That creates a difficult backdrop for policymakers, because inflation risks rise at the same time as economic momentum may start to slow.

- The US is in a stronger position than most regions, but it is not fully protected. Economic growth and business investment are still holding up well, especially where AI spending is involved, but the pressure on lower-income consumers is beginning to build as fuel costs rise and earlier support fades.

- Earnings are still doing most of the work in supporting markets. Strong results from major technology and cloud businesses helped keep confidence intact, although investors are becoming more selective about which AI stories they trust. The overall message remains constructive but more measured: stay invested, but remain selective given higher oil prices, central bank uncertainty and less room for valuation disappointment.

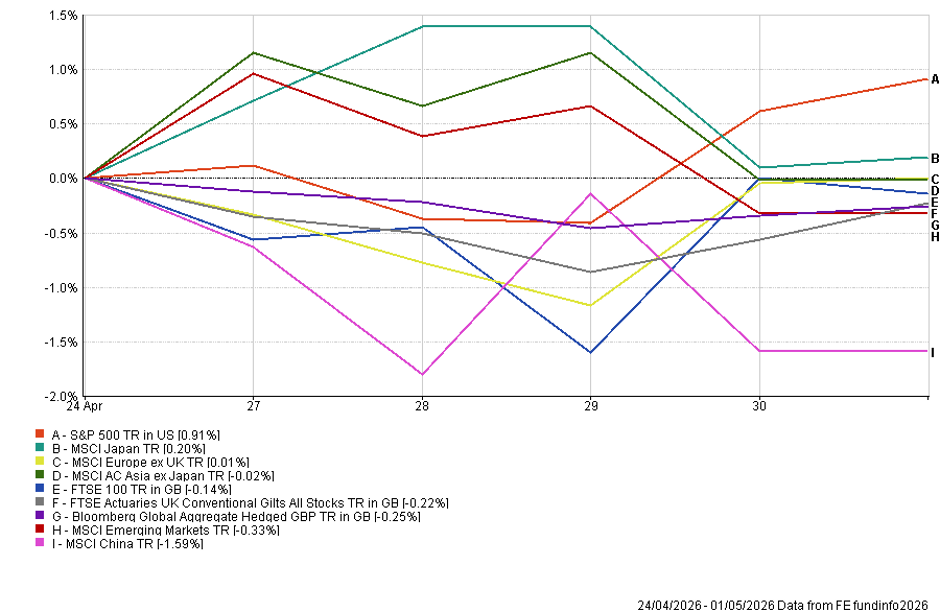

Last week was another reminder that markets do not always behave as the news flow suMarkets remained strikingly resilient last week, even as the Iran war and disruption through the Strait of Hormuz continued to dominate the macro backdrop. The S&P 500 rose to another all-time high, while Japan also made modest progress. Europe, the UK, China, emerging markets and bonds were more subdued, reflecting a familiar pattern: US earnings momentum and technology leadership remain powerful supports, while markets more exposed to energy, weaker growth, or policy uncertainty are finding it harder to keep pace.

The most important issue remains Hormuz. This is not simply another geopolitical headline. The Strait is one of the world’s most important trade arteries, carrying a significant share of global seaborne oil and LNG, as well as key industrial inputs. Shipping flows remain heavily disrupted, with vessels delayed or stranded and no clear confidence that normal traffic can resume quickly. Even with a ceasefire in place, both the US and Iran continue to use access to the waterway as leverage, leaving the route functionally impaired rather than genuinely reopened.

The economic impact continues to build with time. Oil prices remain the clearest transmission channel. WTI traded above $110 during the week before closing near $102, while Brent touched above $120 before ending around $109. Markets are not ignoring this, but equities are behaving as though the shock will remain contained. That may prove right if pressure on Iran forces a deal, but it is a narrow path. Even if an agreement is reached, mines, GPS disruption, insurance costs, naval escorts and shipowner caution could delay any return to normal shipping. Structurally, Iran has shown that Hormuz can serve as a pressure point, suggesting a lasting geopolitical premium in energy markets.

The transmission into the economy is straightforward. Higher oil prices feed into headline inflation first, then into transport, food, chemicals, fertiliser, and wider input costs. It also acts as a tax on consumers, especially lower-income households with limited savings buffers. The initial effect is inflationary, but the second-round effect is slower growth. That is why this shock is so difficult for policymakers. It pushes inflation up while threatening demand later.

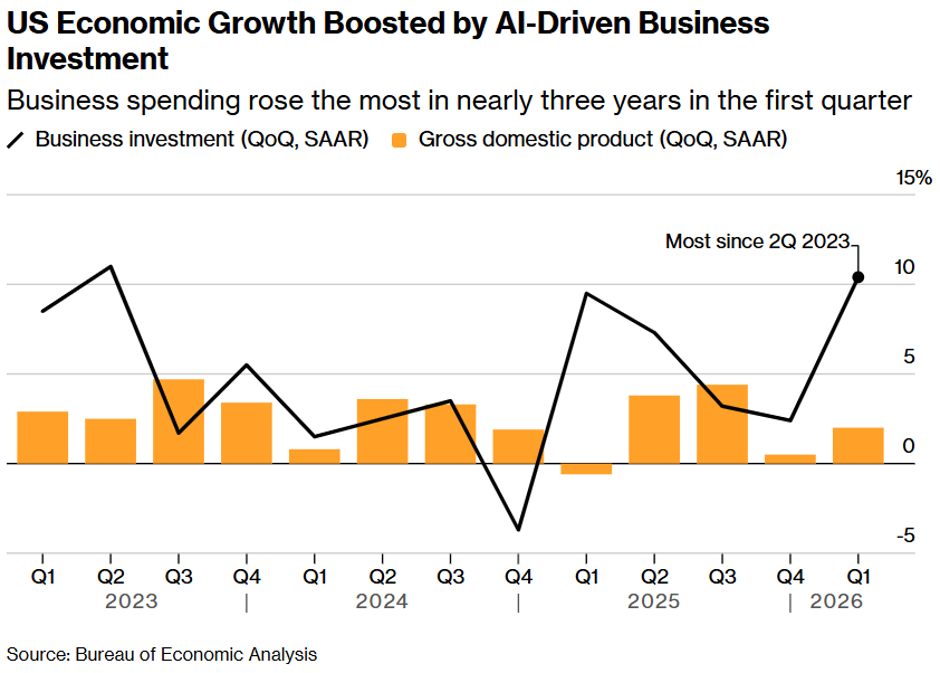

The US is still best placed to absorb the shock. Last week’s GDP report showed the economy growing at a 2.0% annualised pace in Q1, a little below expectations but still consistent with a resilient expansion. More importantly, the detail was better than the headline: underlying domestic demand remained firm, consumer spending grew at a respectable pace, and business investment was notably strong, helped by AI-related spending on data centres, equipment and software. This reinforces the idea that the US is entering the energy shock from a position of relative strength, rather than weakness.

However, the consumer picture is becoming more uneven. Household spending has held up, but higher gasoline prices are already eating into disposable income, particularly for lower-income consumers, while the temporary support from tax refunds is now fading. The stronger part of the US economy remains linked to higher-income households, corporate capex, and the AI investment cycle, while pressure is building at lower income levels. The US is therefore less exposed than Europe or parts of Asia, but it is not immune if energy prices stay elevated for longer.

Last week’s central bank meetings reinforced the point that policy has become more complicated. The Fed left rates unchanged, but the vote split was striking. Three officials objected to retaining the easing bias, while one voted for a cut. That tells us the committee is moving away from a clean disinflation narrative. Powell described the economy as resilient, helped by data-centre demand and investment, but the next move is no longer as obviously a cut as markets had previously assumed.

The ECB also held rates, but Christine Lagarde confirmed that a June hike was discussed. That is a significant change in tone given the weakness of eurozone growth. Europe is caught in the worst part of the trade-off: growth is barely positive, energy prices are pushing inflation higher, and policy flexibility is limited. The ECB may resist the term ‘stagflation,’ but the mix is clearly moving in that direction.

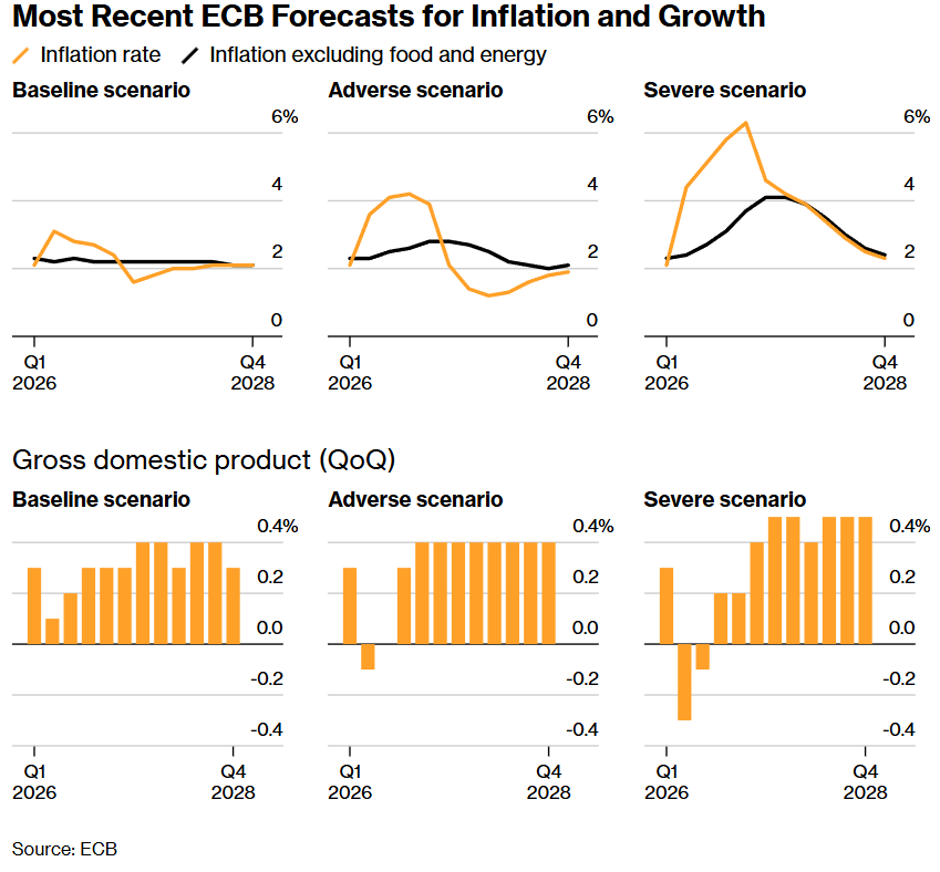

The Bank of England delivered a similarly uncomfortable message. Rates were held, but its scenarios showed the Iran shock lowering real incomes and pushing inflation higher. Andrew Bailey pushed back against the idea that hikes are inevitable, arguing that monetary policy cannot offset a real energy shock. However, the path to rate cuts now looks far less realistic than it did earlier in the year. The UK remains stuck between weak growth and imported inflation, with households likely to feel the squeeze before any policy relief arrives.

Japan added another important market signal. The yen weakened through ¥160 against the dollar, prompting intervention from the Ministry of Finance. The move produced a sharp daily rebound, but the underlying problem remains unresolved. The Bank of Japan has not been hawkish enough to convince currency markets, while Japan is highly exposed to energy flows through the Hormuz Strait. Intervention can slow yen weakness, but a sustained recovery probably requires lower oil prices, lower global yields, or a clearer BoJ tightening path.

Earnings: Against this cautious macro backdrop, earnings remain the main reason markets have held up so well. Big Tech results were central to that. Alphabet was the standout, with Google Cloud accelerating and clearer evidence that AI demand is translating into revenue. Amazon also delivered stronger momentum through AWS, reinforcing the view that the AI infrastructure build-out is creating real demand. Microsoft remains solid, particularly through Azure, although the market wanted more evidence of a decisive step-change in AI monetisation.

Meta was the weaker part of the story. Its increased AI spending raised questions about the timing and visibility of returns, particularly as it lacks the same cloud monetisation engine as Alphabet, Amazon or Microsoft. That distinction matters. The market is no longer indiscriminately rewarding AI exposure. It is starting to separate companies that can turn AI investment into revenue and cash flow from those still asking investors to trust the long-term opportunity.

This does not mean the AI cycle is weakening. Capex plans remain huge, cloud demand is strong, and earnings revisions are moving higher. Roughly 44% of S&P 500 companies reported last week, with results again better than expected. Consensus forecasts for S&P 500 earnings growth in 2026 have continued to rise, and expectations for 2027 also remain strong. Forward earnings are still rising, which is one reason the market continues to climb despite oil and geopolitical risks.

This is the key tension. The stock market balloon is climbing, and the burners are firing. It is not all hot air: earnings revisions, AI capex, large-cap technology strength and improving small-cap participation all provide genuine support. Growth stocks and the Magnificent Seven have reasserted leadership, but the rally has not been entirely narrow, with the Russell 2000 also reaching fresh highs. Sentiment is also not euphoric, which leaves room for markets to keep moving if earnings continue to deliver.

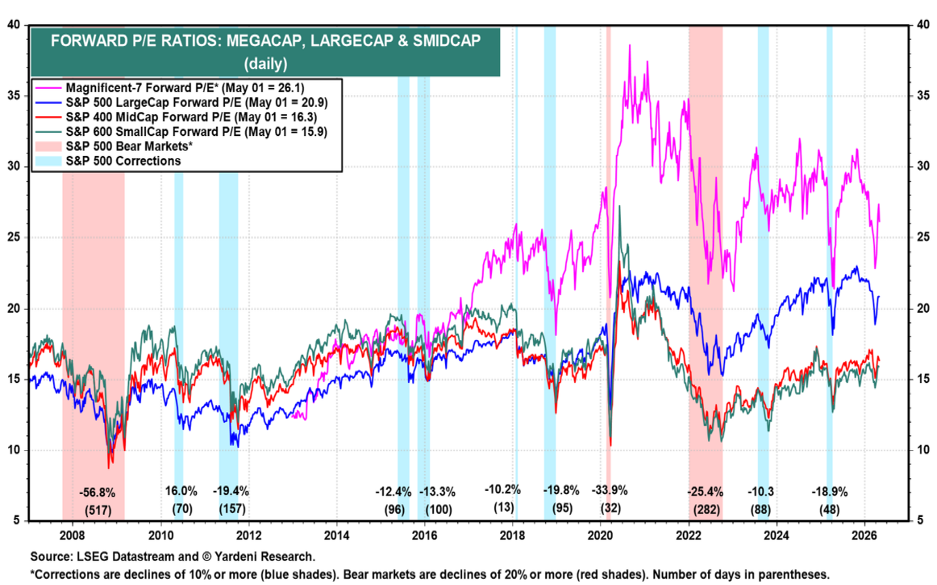

Valuation is the caveat. The market is not obviously in bubble territory, particularly given rising earnings, but it is priced for a favourable outcome. US multiples remain below the extremes seen at the end of last year, and technology valuations are still far from dot-com levels. Even so, the margin for disappointment is thinner. If oil remains elevated, inflation expectations rise further, or central banks push back more forcefully against rate-cut hopes, the market will become more vulnerable.

Bond markets still look relatively relaxed. Short-dated yields reacted to the Fed’s hawkish dissents, but broader fixed income markets do not yet appear to fully reflect the risk that inflation stays higher and that central banks are slower to cut. This supports a continued preference for shorter duration. Bonds can still provide income, but duration is a less reliable hedge when the shock comes from energy and inflation rather than weak demand alone.

This week…

The focus will be on whether the US labour market confirms the resilience implied by equities. This week brings a heavy run of employment data, including JOLTS, ADP, jobless claims, Challenger layoffs, and the April payrolls report. There will also be plenty of central bank commentary, with several Fed officials due to speak. After last week’s split decision, investors will be on the lookout for any signs that the easing bias is being further diluted. ISM services will give a read on domestic demand, while consumer credit will help show whether households are leaning more heavily on borrowing as gasoline prices rise. Productivity and unit labour cost data will also matter, as productivity remains central to the more optimistic outlook. However, Hormuz remains the key macro risk; oil is the main transmission channel; and central banks are no longer comfortably on a path to easier policy. Markets can continue higher, but the risk balance has shifted.

Tom Mcgrath 04.05.2026

Edited Ash Weston 04.05.2026