Market Insight – Markets Begin Pricing Duration, Not Just Danger

We are now entering the third week of the Middle East conflict, and while the military narrative continues to evolve daily, financial markets have begun to shift their focus. The initial phase was about shock. The second was about energy disruption. The third is increasingly about duration and political tolerance. With Brent crude again trading around $100 per barrel, markets are beginning to confront a reality that felt theoretical only a fortnight ago. This conflict has the potential to become an inflation shock rather than simply a geopolitical event.

In simple terms, investors are no longer just reacting to headlines; they are trying to assess how long this environment of elevated oil prices, disrupted shipping routes, and rising geopolitical risk premia might persist. That question is becoming more important than the scale of any single military development.

There are tentative signs that diplomatic channels may be opening at the margins, but for now, escalation remains the dominant trend. Strikes on strategic military and logistical targets have increased the risk of direct attacks on energy infrastructure, while the continued impairment of shipping through the Strait of Hormuz is exerting persistent upward pressure on oil prices.

The Energy Channel Is Now Dominant: The central transmission mechanism from conflict to markets remains energy. Roughly a fifth of global oil supply typically flows through Hormuz, and even a partial disruption has historically had an outsized effect on price expectations. The present situation is complicated further by the decentralised nature of Iranian military capabilities. Even as conventional naval assets are degraded, drone attacks, mines and sporadic strikes on energy facilities can continue to impair supply routes.

This asymmetry means that restoring confidence in shipping security may prove slower than markets initially hoped. Investors are beginning to price not just temporary disruption but the possibility of intermittent instability lasting for weeks or months. That change in mindset matters enormously. Financial markets tend to cope well with short shocks but struggle when uncertainty becomes structural.

Oil’s surge of more than 40% since the start of hostilities is already feeding into inflation expectations. Petrol prices are rising rapidly across developed economies, freight costs are increasing, and the fertiliser supply chain is beginning to show signs of stress. This latter dynamic is particularly important. A prolonged disruption to nitrogen fertiliser exports from the Gulf could translate into weaker agricultural yields later in the year, raising the prospect of a secondary food price shock. Such developments would move the macro narrative from cyclical slowdown risk toward stagflation risk. Bond markets are already reacting to this possibility.

Bonds Are Sending a Clear Warning: One of the most striking market developments over the past fortnight has been the behaviour of government bond markets. If this were a classic geopolitical risk-off environment, sovereign bonds would typically rally as investors seek safety. This time, the opposite has occurred in several key markets.

Yields have risen sharply as investors focus on the inflationary consequences of sustained energy disruption. In the UK in particular, gilts have come under significant pressure. This reflects a growing recognition that higher imported energy costs can push inflation higher even as growth slows — a combination that central banks find especially difficult to manage.

The sell-off in bonds is therefore not just a technical move but a macro signal. Markets are beginning to contemplate the possibility that central banks may be forced to delay or even reverse easing cycles that were widely expected only weeks ago.

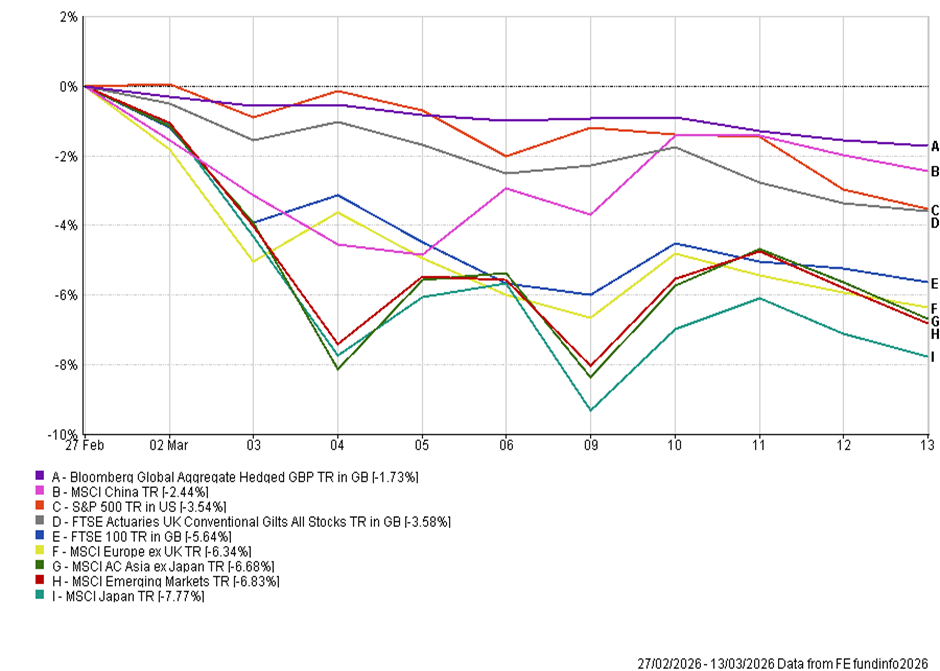

Equity Markets: Equity market performance since the first strikes illustrates a familiar hierarchy of resilience. US equities have held up comparatively well, supported by dollar strength, domestic energy production and the concentration of large, globally diversified companies within the index. China has also been relatively stable, reflecting both policy support and lower direct exposure to Middle Eastern supply routes.

By contrast, Asia ex-Japan, emerging markets and parts of continental Europe have experienced deeper drawdowns. Japan has also struggled amid currency volatility and higher input costs, which weigh on investor sentiment. The FTSE 100 has not been immune either, despite its energy-sector exposure, as rising gilt yields and domestic growth concerns have offset the benefits of higher commodity prices.

However, resilience in US equities should not be mistaken for complacency. Political pressure is now beginning to build domestically as higher gasoline prices feed directly into household budgets. The US consumer is often portrayed as remarkably tolerant of external shocks, but rising fuel costs have historically been among the fastest ways to erode confidence and political goodwill.

As one strategist put it succinctly this week, “the US market has been more resilient, but Washington’s political clock may now be moving faster than the military one.” That observation captures the core risk. Military objectives can be pursued over months. Political patience often cannot.

US Macro Backdrop: Improving Before the Shock: Ironically, the United States’ inflation backdrop had been gradually improving before the escalation. Underlying price pressures eased in February, with core inflation holding at its slowest annual pace in several years. Housing costs moderated, goods price inflation remained subdued and real wages showed tentative signs of recovery.

In a different environment, such data might have reinforced expectations of monetary easing later in 2026. Instead, the energy shock has complicated the policy outlook. Rising oil prices risk pushing headline inflation higher in the near term, even as labour market indicators soften. This leaves the Federal Reserve facing an increasingly uncomfortable trade-off between growth risks and inflation credibility.

Markets have already responded by pushing back expectations for rate cuts. The central bank is unlikely to signal aggressive easing while inflation uncertainty remains elevated. Policy inertia, rather than policy support, is therefore becoming the dominant theme.

UK Weak Momentum Meets External Shock: The UK enters this phase with a fresh bout of relative fragility. Recent data showed economic activity stagnating at the start of the year, suggesting limited underlying momentum even before the conflict intensified. Weakness in recruitment activity, subdued services output and declining housebuilding all point to a growth outlook that was already vulnerable.

Higher energy prices now threaten to compound these pressures. Fuel costs are rising, mortgage pricing is adjusting upward, and sterling has weakened against the dollar as global investors rotate toward perceived safe havens. The risk is that the UK faces a combination of slowing growth and renewed inflation pressure — a (familiar) uncomfortable scenario.

Looking Ahead Policy Meetings Overshadowed: Central bank meetings in the UK and euro area will attract attention in the coming days, but they are unlikely to alter the broader narrative. Inflation risks linked to energy prices mean policymakers are expected to remain cautious. Even if growth data weakens further, the willingness to ease policy aggressively while oil prices remain elevated is limited.

Instead, markets will continue to focus on tangible indicators of de-escalation. Evidence that shipping routes are reopening, energy supply disruptions are stabilising or credible diplomatic negotiations are advancing would likely provide the first meaningful catalyst for improved sentiment. Until then, volatility is likely to remain a defining feature of markets.

Staying the Course: Periods like this inevitably feel unsettling. Headlines are dramatic, price moves are sharp, and uncertainty appears unusually high. Yet history suggests that geopolitical shocks, while capable of triggering corrections, rarely derail long-term market trends unless they evolve into sustained economic crises.

There are already signs that long-term investors are beginning to re-engage selectively at lower levels. Valuations in several markets have adjusted meaningfully, and liquidity conditions remain broadly supportive. Importantly, the underlying drivers of global growth – technological investment, productivity gains and structural capital expenditure cycles – have not disappeared.

Written by Tom McGrath 15.03.2026

Edited by Ash Weston 15.03.2026